What You’ll Learn

Federal and lender-specific FHA loan requirements

How to determine if an FHA loan would be beneficial to you

Finding the type of loan that fits your financial goals is one of the most important parts of the homebuying process. Payback periods, rates, and down payment minimums can all fluctuate with different loan products and have an enormous impact on the overall affordability of your mortgage. FHA loans are a popular choice (especially among first time homebuyers) because they offer more flexibility when it comes to debt, savings, and credit scores.

The FHA, or Federal Housing Administration, is one of several government agencies that insures loans, making it possible for approved lenders to offer financing options to a wider range of borrowers. (Other agencies that insure loans include the Department of Veteran Affairs with VA loans and the US Department of Agriculture with USDA loans.)

FHA loans are all about accessibility, and can be a great option for borrowers with lower credit scores and/or smaller savings. Because the government is backing these loans, the qualifying standards are more lenient. While you can use a FHA home loan for purchasing or refinancing a home, this article will focus on FHA loan requirements for buying your first home.

How to qualify for a FHA loan at a glance

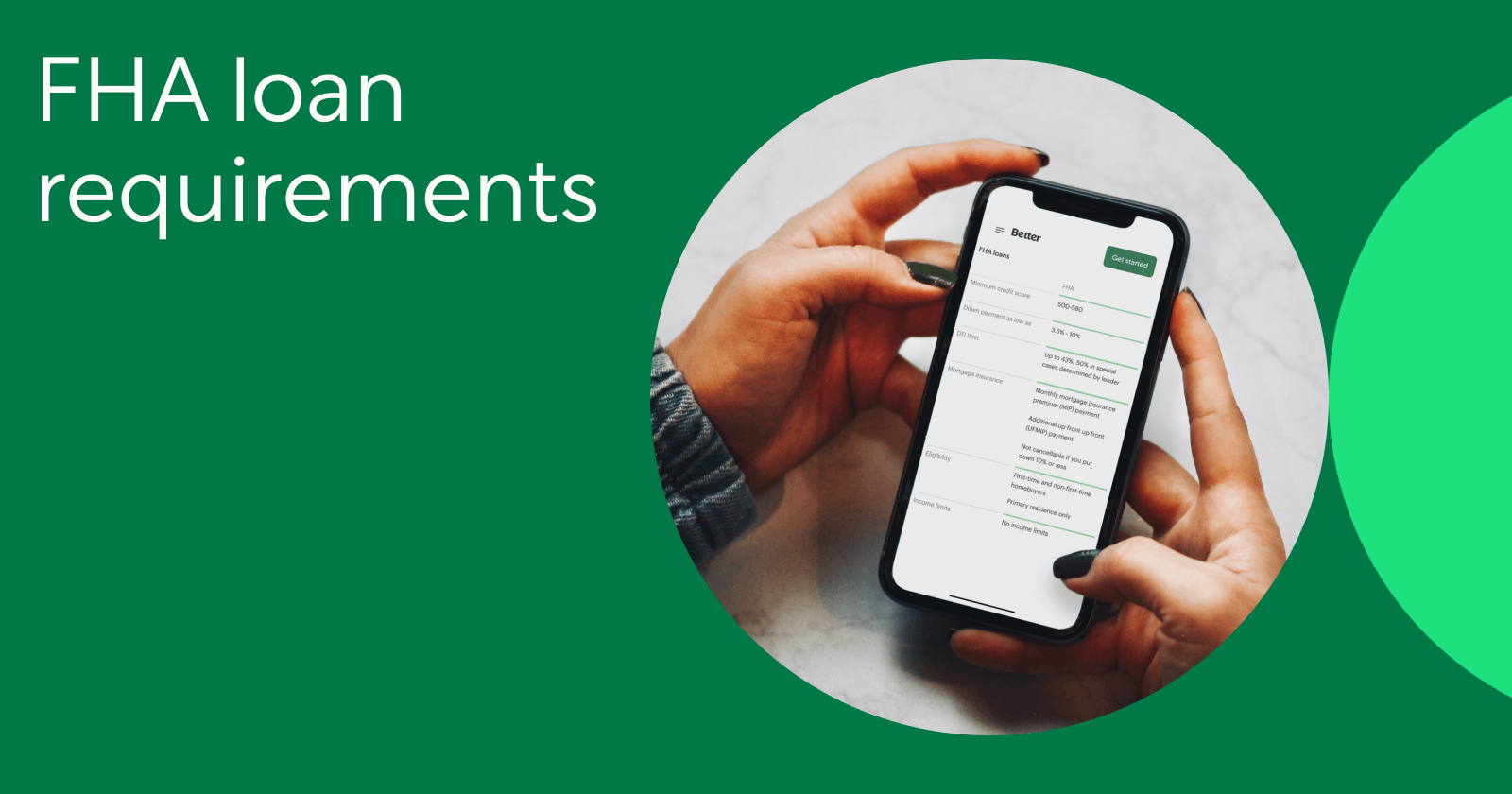

FHA loans are guaranteed by the government, but the funding itself comes through FHA-approved lenders. That means you’ll still need to apply for your FHA loan directly through an approved lender (like Better Mortgage) just as you would for a conventional loan. The FHA has set these minimum qualifying guidelines for applicants:

A minimum down payment of 10% if your credit score is between 500-579 OR

A minimum down payment of 3.5% if your credit score is above 580

Evidence of steady income and proof of employment

MIP (Mortgage Insurance Premium) payments

A debt-to-income ratio of 43% or less

The home in question must be your primary residence

The property must meet FHA-specific appraisal requirements

FHA loan maximums apply to certain properties and locations

These minimum qualifying guidelines are a helpful framework for understanding the general parameters of FHA loans, but the exact requirements can vary from lender to lender. You may have trouble qualifying for an FHA loan if you have insufficient credit history, a track record of making late payments, outstanding debt, or any recent foreclosures or bankruptcies. Each lending institution ultimately has the final say when it comes to approving borrowers based on their unique evaluation criteria.

The minimum FHA loan credit score

Your credit score is a snapshot of your past actions as a borrower. When you apply for a conventional mortgage, lenders look at your credit score to get a sense of how likely you are to pay back your mortgage debt on time. Higher credit scores indicate that you have a stronger track record of repayment and tend to qualify your loan for more favorable interest rates.

When it comes to FHA loans, lenders are more lenient in their credit score scrutiny. Borrowers with credit scores 500 or higher can qualify for an FHA loan, though their exact credit score will impact their down payment requirement and minimums vary from lender to lender. FHA standards stipulate that borrowers with a credit score between 500-579 can qualify for a 10% down payment, while borrowers with a credit score of 580 or higher can qualify for a 3.5% down payment—stronger credit scores come with a low down payment advantage. At Better Mortgage, the minimum credit score requirement for FHA applications is 580.

FHA loan down payment requirements

Saving enough money for a down payment can be daunting. This one-time cost is due in full at closing, and the size of your down payment can impact the long-term affordability of your mortgage—for example, smaller down payments on a conventional loan might mean higher interest rates, but bigger down payments can easily drain borrowers with limited savings. Government loans provide a solution for borrowers in this position. With an FHA loan, the rules of down payments are slightly different. Most importantly, you can qualify for competitive rates and loan terms with as little as 3.5% down payment.

Having said that, a larger down payment still has benefits, even in the world of FHA loans. For example, a 10% down payment might help offset a poor credit score more effectively than a 3.5% down payment, while also qualifying you for slightly more competitive rates and even increasing your chances of getting approved. Another benefit of FHA loans is that your entire down payment can be derived from outright gift money, so long as the money comes from an FHA-approved source and you can verify there is no expectation of repayment from the giver. This is a significant departure from conventional loans, which have strict rules around supplementing your down payment with gift money.

FHA debt-to-income ratio requirements

Your debt-to-income (DTI) ratio is an important factor no matter what type of loan you’re getting, but it needs to be at or below 43% in most cases to qualify for an FHA loan (50% limits are accepted in certain situations depending on your lender.) DTI is a standardized way of comparing your income to your debts, and can be calculated by dividing your monthly debt payments by your gross monthly income. So a 43% DTI ratio basically means that for every dollar of monthly household income you earn, 43 cents goes off to paying for your debts. This measurement gives lenders an understanding of your other ongoing financial obligations, and helps to determine whether taking on a mortgage in addition to those debts is reasonable. A lower DTI will likely qualify you for more favorable loan terms.

FHA loan income requirements

There are no maximum income limits for FHA loans, which means making a certain amount of money won’t disqualify you from eligibility. You will need to provide evidence of steady income and proof of employment—lenders generally want to see at least 2 years of consistent job history, which is a standard guideline with all loan applications. FHA lenders use your employment to confirm your ability to pay back your mortgage, which is why they also evaluate your debt-to-income ratio. In this case, the amount of money you take home is less important than the portion of that income earmarked for other debt.

FHA maximum and minimum loan limits

There is no minimum loan limit, but there is a maximum limit when it comes to the amount you can borrow with an FHA loan. That max amount depends on where you live and the type of home you’re purchasing. You can use this tool to see the specific FHA loan limits for your county, but loan limits are generally informed by the surrounding property values and a certain area’s cost of living.

FHA mortgage insurance premium

Like most mortgages with less than 20% down payment, FHA loans include insurance fees. In this case, these fees are mortgage insurance premiums (MIP), which are paid once at closing and then monthly throughout the life of the loan. The exact cost of FHA monthly mortgage insurance depends on variables like loan amount, length of payback period, and down payment size; most borrowers will pay anywhere from 0.50%-1.50% of their loan amount per year. This annual sum will be divided up and baked into your monthly mortgage payments, so when you’re calculating the affordability of your loan make sure you account for this additional cost.

FHA borrowers will also pay a one-time upfront mortgage insurance premium (UFMIP), equivalent to 1.75% of the total loan amount. This can either be paid at closing or rolled into the cost of your loan and spread out in smaller payments over time. If your down payment on an FHA loan is more than 10%, you can request to cancel MIP payments after 11 years; if your down payment is less than that, MIP is never cancellable. It’s possible that refinancing your FHA loan into a conventional mortgage down the line could reduce or eliminate insurance fees altogether, but you’d need to calculate the costs and determine whether the breakeven point makes financial sense for your goals.

FHA minimum property standards

When you’re buying a home with an FHA loan, the property itself also needs to meet certain eligibility criteria. This means that the appraisal process for a FHA loan is more stringent than the appraisal process for a conventional mortgage loan. Essentially, the government wants to be sure that the home they’re helping you finance meets basic structural and safety standards. This protects lenders from investing in poor quality homes, and it also protects FHA borrowers from buying homes in need of significant repairs or renovations that might become financially unmanageable, check out the HUD’s Single-Family Housing Policy Handbook for more guidance on the FHA property appraisal process.

Steps to getting approved for an FHA loan

Instead of placing a lot of emphasis on credit score and savings, lenders tend to focus more attention on verifying consistent income when evaluating FHA loan applications. You’ll need to gather some key documentation including:

Proof of residence

Social security number

Valid government-issued identification

Valid W2 and tax forms for the past two years

Rather than providing a way to fund rental or investment property, FHA loans are meant to help make homeownership more accessible for more people. So, on top of proper documentation, you need to confirm that the place you’re planning to purchase with your FHA loan is a primary residence.

Apply for an FHA loan online today

FHA loans tend to be a good fit for borrowers looking to avoid the big upfront costs of homebuying. These loans are also an alternative for borrowers who might not qualify for a conventional mortgage based on their credit score. There are some additional costs associated with FHA loans (namely, ongoing insurance premiums) that you’ll need to consider when deciding whether FHA is a good fit for you in the long-term. But if your priority is finding a path to homeownership, government backed loans might be the most feasible way forward.

At Better Mortgage it’s our mission to make homeownership more accessible to everyone, which is why FHA loans are currently available to purchase customers in all states where Better Mortgage is live. Never worry about predatory fees, easily compare rates 24/7, and find the mortgage that works for you. Our simple online tools make it easy to get pre-approved in as little as 3 minutes and explore your options.